The pharmaceutical industry enjoyed a long period of superior financial performance. That period seems to be over. Current Big Pharma challenges can be summarized as follows:

- Increasing cost of drug discovery & development due to …

- tougher regulatory demands

- competition for patients

- larger clinical studies

- high rate of failures

- new technologies not yet paying out (genomics, …)

- longer development timelines

- Increasing time to market. For instance, a delay in the launch of a drug can cost a company up to $ 23 million per day in terms of lost sales in the USA alone and almost $37,000 per day in terms of additional development costs [1]

- Impending patent expirations of blockbuster molecules. For example, drugs worth $20 billion went off – patent in the US in 2008, similar the years before; 2011 $30 billion sales faced generic competition in major markets)

- Challenges to intellectual property by increasingly aggressive generic companies

- Pricing pressure in US and Europe (by governmental pressure reducing health care cost)

- Increased penetration of generics

- Considerable reduction in the numbers of new product approvals (FDA approvals: 2007/18; 2008/22; 2009/25; 2010/21 – constant on low level; in 2007 lowest in 24 years)

- Re-importation pressures

- Low public opinion

All this means pharmaceutical multinational companies (MNCs) have to radically rethink their strategic options and business model: how to defend revenue, how to increase productivity, how to lower unit cost.

One way out is to look out towards Asia for solutions - not only with respect to manufacturing or support services but also research and development. Offshoring R&D has already proven beneficial and even essential in comparable high-skill industries such as the software industry. Global resourcing of R&D can help pharma companies to unlock significant productivity gains.

Subsequently, the center of the global pharmaceutical industry is shifting. Not only is Asia set to become the largest pharmaceutical market in the world but many Asian territories will be powerhouses of the industry. The shift started as Asian economies grew and low-cost manufacturing in the region expanded. Now, Western companies are increasingly seeking site research, development, analytical services and clinical trial activity in Asian territories. This reflects both increased capabilities in the region and a changed business model of MNC. The sheer size and purchasing power of patient populations in emerging Asian healthcare markets, combined with improving regulatory and business environments, is attracting Western pharmaceutical companies. In terms of population and economic expansion, there is no doubt that the 21st century is dominated by Asia. At 4 billion people (60% of world population), the Asian population is predicted to grow to 5 billion people by 2050. Although politically and culturally diverse, all major Asian countries are working hard to open their economies and create a conductive business environment. The view that the center of the pharmaceutical industry is moving away from North America and Europe and towards Asia is shared by pharmaceutical MNCs and Asia-based companies alike. 50% of MNCs agreed with that statement and less than a quarter voiced any disagreement with the prospect of such a shift [3].

In 2008, the global pharmaceutical market was worth $ 773 billion, growing by about 5% over 2007, according to IMS. The Asia/Africa/ Australian region has had the highest growth rate of 15.3% to $90.8 billion over 2007, as compared to North America at 1.8% and Japan 2.1% [4].

Historically, the pharmaceutical industry has been slow to embrace offshoring, but over the last decade this trend has begun to reverse with significant movement to global sourcing. Unlike many other industries, the pharmaceutical sector is uniquely positioned to remotely execute one of its core competencies, i.e., R&D, which represents 74% of offshored employment [5].

Part of that change is the recognition that one of the key challenges of the biopharmaceutical industry is to improve R&D productivity, i.e., to deal with the lack of innovative molecules in the pipeline, increasing pressure from the governments to reduce healthcare expenditure, and the rising cost of regulatory activities. Development organizations are targeting the drivers of cost and value aiming to increase R&D productivity through a series of lines of attack. Offshoring is one such approach.

In other words, an essential element of retooling the R&D engine is to offshore R&D – especially to Asia. For obvious reasons such as strategic importance and market size, the Asian countries of choice are particularly China and India. Background for offshoring, opportunities and risks in conducting R&D in Asia, and in particular the India option, have been explored in a multi-part publication in Chemical Weekly [6], and in various other recent publications by the author of this article [7-10].

India, China and Singapore are poised to become leading countries in the Asia pharmaceutical space. Other territories, notably South Korea, Malaysia and Thailand are also building strong domestic pharmaceutical bases although so far only MNCs currently dominate these markets.

For example, China has leapfrogged major European markets and is on its way to become the world’s fifth-largest national market for prescription pharmaceuticals, with current sales of approximately $25 billion. It is no wonder that many MNCs are intensifying their market efforts, investing ever more deeply in commercial operations. But alongside this commercial activity, the pharma scene in China and India is also buzzing with R&D activity.

The quick and easy justification for investing in R&D activities in China and India would seem to be the cost factor. As is well known, increased developmental cost up to more than $1 billion are contrasting the pressure by health authorities to decrease prices. From this perspective a cost-driven shift towards outsourcing to low-cost countries, particularly to Asia, is observed. The consulting firm Arthur D. Little predicted in 2004 that pharmaceutical outsourcing (including offshoring) in US would become a $48 billion business in 2008 [11]. In reality, it became a $ 168 billion business by 2009 [12]. Consequently pharmaceutical MNCs expect that just relocating lab work and even more clinical trials from the West will halve wage bills, rentals and overhead.

However, offsetting costs arise from relocating the necessary Western staff, importing equipment and supplies and ensuring maintenance of equipment, in addition to the impact of possibly lower productivity and security, differences in technical practices, regulatory and legal requirements, culture and language.

However, cost savings alone are not the primary consideration for the pharmaceutical industry. Because of the expected rise in wages of high-skilled employees, increasing costs of support functions and compliance in Asia, focusing on cost advantage will be a short-sighted view.

The real and true value of conducting pharma R&D in India and China lies elsewhere - as a strategic lever for helping companies achieve their Asian ambitions. Very broadly, the more R&D that MNCs conduct in India and China, the more opportunity they have to increase their visibility and reputation. This will help them to reshape domestic healthcare markets as well as consolidate their own position.

In a nutshell, smart R&D offshoring can serve many purposes in the pharmaceutical industry:

- By providing early access to emerging markets

- By supporting MNCs sustainable growth in big Asian economies, i.e., the more R&D MNCs conduct business in Asia the more opportunity they have to shape the future of the Asian health-care market and to consolidate their own position within it

- By accelerating launches, e.g., by tapping into large and naive patient populations

- By accelerating enrollment into clinical studies

- By building new growth platforms

- By enriching pipeline

- By capitalizing on Asian talent pools and innovation development potential

- By utilizing “reverse brain drain” by hiring returnees in the respective Asian countries

- By leveraging on highly developed IT and bioinformatics (India) All of the above results both in improving global cost structure and counterbalancing reduced growth rates in the West.

Still, the most prominent subject in pharmaceutical R&D, clinical trials, needs to be mentioned in the context of the ongoing R&D shift towards the East. It is this type of R&D activity that absorbs most of the dollars. The number of clinical trials has risen tremendously over the past few years. Between the years 2005 and 2006 alone, clinical trials conducted in Asian-Pacific countries increased by 50% [13]. In addition to significantly lower clinical research costs, the region offers the advantage of a massive, genetically diverse population, many of whom have never been treated for their condition. Thus, subject recruitment is easily facilitated, and the enrollment requirements are more readily met.

Lastly, another at least equally important aspect must be mentioned. This is the significant and almost indefinitely expandable talent pool. In addition to having a large output of high-quality, locally trained scientists, India and China have an impressive and steadily increasing number of scientists who have returned in recent years with Master’s and Doctoral degrees earned overseas.

The fact that the Intellectual Property Rights (IPR) situation was adapted to the international standard (with India recognizing full product patents on pharmaceuticals in 2005; China’s entry into World Trade Organization, WTO, in 2001) has further enhanced the dynamic in setting up a strategic R&D presence of pharmaceutical MNCs.

Why is sufficient patent protection in India and China so important? Firms in these countries are important suppliers of low-priced API’s and increasingly finished products domestically, to developing countries and (in particular India) also to the West. There has been a fear that the introduction of product patents will destroy these industries and lead to increased drug prices in the importing countries.

Yet the impact of the changed patent regime is much broader. Besides access to new medicines in India and China, changing IPR is influencing the business strategies of Indian and Chinese firms and their incentive to invest in R&D in order to move up the product/market hierarchy. Furthermore, Western MNCs operating in those countries (may that be by selling their products as well as by investing in a local presence in either R&D or manufacturing operations) are highly affected.

The IPR situation in China is still perceived as “tricky.” Nevertheless, MNCs are further establishing or expanding their presence in China, allowing them to also test the conditions of the market and establish relationships for the future.

In particular, India API manufacturers provide evidence that confidence is building and Western pharma companies are now bringing more sensitive projects to India. However, India still has a reputation of relatively weak IPR protection in terms of enforcing its legislation.

While perceived as an issue, IPR protection is a decreasing barrier to offshoring R&D activity. In particular, these potential types of offshored R&D activities related to chemical and pharmaceutical development, are generally less affected. To illustrate: upscaling and optimizing an API manufacturing process for an NME, formulation development, analytical method development and validation, as well as running analytical stability studies, all typically occur in a late stage of the R&D process, long after completed patent protection of a new molecule. Furthermore, they are generally less related to IP origination.

Based on the information available in public domain (and on personal experience), there have not been any IPR issues or violations occurring across industry in that area up to now. With proper contractual agreements in place and the careful selection of a reputed vendor, this danger may be effectively managed. One should understand that for major pharmaceutical firms (especially in India), who make significant efforts to establish themselves as key players in the international pharma market, infringing on the intellectual properties of the customer is not in the best interest of the service provider.

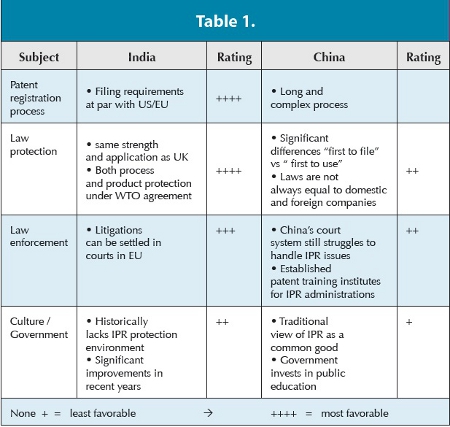

Overall there is no doubt that India has a more mature legal system for IPR protection than China. However significant practical issues still exist in both countries. While the risk for legal aspects such as patent registration process, patent law coverage/protection and information disclosure requirements by customs/ government in India is considered low, this risk is higher in China.

The risk for practical aspects such as law enforcement, legal system efficacy, and support of overall environment (IPR track record, governmental policy, business environment and culture) is medium in India but rather high in China.

Findings from a study executed a few years ago are summarized in Table 1.

In summary, there are myriad reasons why most pharmaceutical MNCs migrate East including: strategic presence facilitating growth in emerging huge markets, cost savings, utilizing Asian talent pools, access to abundant preclinical animal resources (China) and drug-naïve patient population, capacity constraints in the West and, lastly, taking advantage of developing products for local markets in close proximity to their customers.

To illustrate the impact of the emerging Indian and Chinese pharmaceutical powerhouses: 80% of the currently used APIs for drugs made in Europe are manufactured in India and China [14]. It is easy to predict that finished drug products will soon follow.

Although the pharmaceutical industry came late into offshoring, pharma stands to benefit at least as much as other industries from the opportunities that offshoring presents. The real value lies not only in cost savings but also in the faster development of new compounds and in penetrating huge new markets. Nowadays, offshoring means looking beyond simple labor cost savings.

Currently, the global pharmaceutical industry is seriously embracing the advantage of offshoring and general expansion towards Asia, i.e., to India and China, both huge potential markets and low-wage powerhouses. The reality of shrinking profit margins, drying pipelines, patent expirations, intense generic proliferation and increased R&D costs has made offshoring an attractive strategy. In particular, R&D activities come into focus of MNCs. Next to conducting clinical trials (which are 80 to 60% of a NME’s development costs) and API-related activities such as chemical process research, increasingly full end-to-end R&D activities are about to be set up by MNCs in Asia. Multifold business models are applied, mostly by acquiring local companies, strategic partnerships and increasingly, by setting up wholly-owned R&D centers.

Despite all of these advantages, outsourcing to Asia introduces new complications that must be addressed, including differences in regulatory procedures, infrastructure, medical practices, language, and culture. Although some of these factors are well-understood, the importance of language is commonly underestimated. Likewise, Western MNCs are correct to be wary of offshoring sensitive and vital operations. There is low tolerance for error industry-wide; simple mistakes can compromise results, or even harm patients, resulting in massive and expensive liability.

The cost of an unsuccessful partnership is more than just a financial issue as the company loses crucial time and opportunity that could have been invested elsewhere. In the case of offshoring via outsourcing to a third party, there is also a loss of partial control as it passes from client to provider. Poor communication can lead to problems with quality and delays. Intellectual property questions need to be addressed on a case-by-case basis. Finally, working across multiple languages and time zones is introducing extra complexity.

Given the objective constraints in the pharmaceutical industry, the globalized world, and the importance of newly emerging markets, offshoring and expansion towards Asia is simply unavoidable, regardless of the means and business model. Delivery of offshoring benefits requires, besides sustained investments and development of management experience, in particular endurance and adaptability to cross-cultural differences – this all in line with the pace of capability development in individual geographic Asian environments.

There are few who have not yet realized that offshoring of significant amounts of R&D, manufacturing, and any other type of core and non-core competencies is becoming an integral component of sustaining profit levels. Very few major pharmaceutical companies do not have pilot programs in place or do not have plans to offshore sizeable components of their operations. Offshoring is expected to increase by 16% annually, driven by robust increases in the augmentation and relocation of both back-office procedures and core processes as R&D [15].

References

1. Datamonitor (2008)

2. Datamonitor (2008)

3. PriceWaterhouseCoopers, Gearing up for a global gravity shift (2007)

4. IMS Health Market Prognosis, March (2009)

5. R. Pascal and J. Rosenfeld: The Demand for Offshore Talent in Services, Washington D.C., McKinsey Global Institute Press (2005)

6. F.U.Floether: Offshoring of Chemical & Pharmaceutical R&D to Asia, Chemical Weekly April 14 (part 1) , April 21 (part2) and April 28 (part 3) (2009)

7. Floether, F.U., How to identify the right partners in Asia-Pacific? Pharmaceutical Technology Europe, September (2010)

8. Floether, F.U., Unlocking the value of your strategic partnerships with CRO‘s and pharmaceutical companies in Asia Pharma IQ Newsletter, March (2011)

9. Floether, F.U., Aspects to be considered by Western MNCs before creating their Asian presence The Pharma Review, March-April (2011)

10. Floether, F.U., Pharmaceutical R&D goes Eastchimica oggi / Chemistry Today –vol.29 n.4 July /August 2011 – Focus on CRO/ CMO’s

11. Arthur D. Little: S. Viswanathan, Are you moving out ? Pharmaceutical Formulation & Quality (2004)

12. ReportLinker (2011) http://www.reportlinker.com/p047598/ Contract-Research-and-Manufacturing-Services-India-CRAMS.html

13. Thomson CenterWatch, Nov (2007)

14. H. Prinz und C. Schulz, Vergleich des EG-GMP Leitfadens Teil I mit der SFDA-GMP Guideline fuer Chinesische Firmen, Pharm. Ind. 70 Nr. 9 (2008)

15. D. Farrel (editor), The Emerging Global Labour Market, Washington D.C., McKinsey Global Institute Press (2005)

Frank U. Floether has an educational background in chemistry and pharmacy. He received his Ph.D. in chemistry in 1977 and in pharmacy in 1989 from the Martin-Luther-University Halle- Wittenberg, Germany. He has served as Executive and Senior Executive for more than 30 years in pharmaceutical R&D, both in generics and in multinationals such as Johnson & Johnson. Prior to retirement, Dr. Floether was VP Global Analytical Development (2001-2005), and VP Business Development, Asia-Pacific(2005-2008). Frank gained broad international experience in Germany, Switzerland, Belgium, India and the United States. He has contributed significantly to the expansion of pharmaceutical R&D capacities for Johnson & Johnson Asia. He remains active as a consultant advising on outsourcing of pharmaceutical R&D to Asia and assisting in setting up alliances between Western and Asian pharmaceutical companies. The author is a member of various scientific advisory boards at European and Asian companies and a lecturer at the Swiss Federal Institute of Technology in Zurich, Switzerland. Frank is inventor/co-inventor or author/co-author of more than 60 patents, scientific papers and books. His most recent contribution is a co-authored book titled, “Strategic Alliances in Biotechnology and Pharmaceuticals” (Nova Publishers, New York, USA, 2010). For more information, please go to www. floether.ch.